February 12, 2015

Puerto Varas, Chile

Twenty-seven years ago at the 1988 Republican National Convention in New Orleans, George H. W. Bush accepted his party’s nomination to run for President of the United States.

(This was when he announced Dan Quayle as his running mate, to which Senator John McCain later remarked “I can’t believe a guy that handsome wouldn’t have some impact.”)

In his acceptance speech, the elder Bush famously told America that he wanted a “kinder, gentler nation.”

It took nearly three decades, but it seems that his wish has finally come true. Sort of.

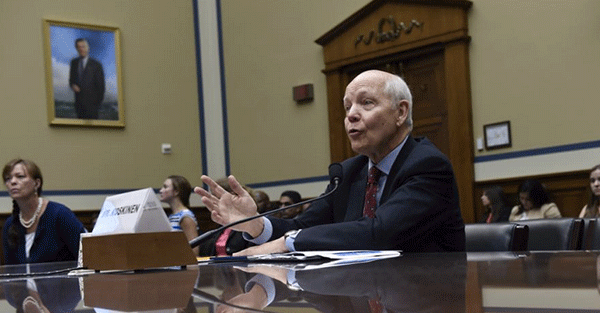

Yesterday afternoon, the Commissioner of the Internal Revenue Service appeared in front of the House Way and Means Oversight Subcommittee… and apologized to taxpayers, specifically those who have had their assets seized and bank accounts wrongfully frozen.

He actually used that word.

“To anyone who is not treated fairly under the [tax] code, I apologize.”

This is pretty astounding.

You see, in the Land of the Free, the Internal Revenue Service, along with hundreds of other state and federal agencies, have the power to seize your assets and freeze your bank accounts, almost instantly in many cases.

You don’t need to be convicted of a crime. You don’t even need to be doing anything illegal.

If you (or your assets) are simply at the wrong place at the wrong time… or if someone so much as suspects that maybe, just maybe, you might be doing something wrong, your assets can be frozen.

Bear in mind, this isn’t anything that goes to court. No one puts you on trial or gives you the opportunity to defend yourself.

It’s a purely administrative action. They just go and do it. And they’re not shy about using their authority.

One case highlighted in front of the subcommittee was of Mr. Andrew Clyde, a gun-shop owner in Athens, Georgia.

Mr. Clyde’s is an obvious criminal terrorist whose heinous, immoral act against society was making a series of deposits into his bank that were all less than $10,000.

His bank viewed this as potentially suspicious activity; US law requires banks to report deposits of more than $10,000. But if they see customers routinely depositing amounts less than that, they assume that customers are doing this deliberately to avoid reporting requirements.

This assumption alone can cause many banks to snitch on their customers, tipping off the IRS that something ‘suspicious’ is happening.

This is all the IRS needs to seize people’s assets. And, once frozen, citizens must go through lengthy and expensive battles to get back their money.

In many cases, it’s not even worth the fight. There’s no guarantee of success. And even if someone gets robbed of $100,000 or more, it might not be worth spending 2-3 years away from running his/her business to get the money back.

The cost of doing so would be greater than the reward of recouping the lost cash.

But here’s the even bigger irony: the IRS believes that if people don’t step forward and fight them, then it is a de facto admission of guilt.

In other words, only criminals don’t fight to get their money back. Only the guilty make a rational cost/benefit analysis in determining whether they should indefinitely neglect their businesses and wage an expensive and uncertain legal battle against the most intimidating organization in US history.

So despite the rather hollow apology from the IRS, it’s clear these guys still need a reality check.

One key lesson to highlight here:

If you hold savings at a bank in the United States, you need to understand that your bank is an unpaid spy of the federal government. They WILL report you for anything you do that they view as potentially suspicious.

Moreover, they are required by law to file a certain number of ‘Suspicious Activity Reports’ each year. So even if you’re not doing anything suspicious, if you simply stand out a bit more than the next guy, you’re going to get reported.

Oh yeah, they won’t tell you about it either.

Bottom line, even if you’ve never broken the law, you could potentially be frozen out of your savings. No one ever believes it will happen to them… until it does.

So make sure you have at least some form of savings somewhere else. Establish a foreign bank account. Hold some gold at a private, non-bank facility. Or even build up a small stash of cash savings.

This way, should the worst happen, you’ll at least have access to some emergency savings to tide you over.