Value Investing:

Step-by-Step guide to one of the most successful investment strategies in the world

-

AUTHOR

Tim Staermose -

LAST UPDATED

May 23, 2019

[Editor’s note: This article was written by Tim Staermose– Sovereign Man’s Chief Investment Strategist and editor of our flagship investment service, the 4th Pillar.]

John Templeton is often considered one of the most successful investors of his generation.

At the height of the Great Depression in 1930, he bought 100 shares of each company listed on the NYSE that was trading for less than a dollar.

He thought that eventually the bad times would pass. And stocks were the cheapest they had been in fifty years.

So he loaded up. As America emerged from the depression, Templeton became a wealthy man.

Later in his career, he realized the massive opportunity for growth in emerging markets, and dedicated a large part of his life looking for overlooked, undervalued opportunities abroad.

He strongly believed in taking profits when expectations and valuations reached unreasonable levels. For example, he sold the majority of his stocks just before the dotcom crash, and then again before the 2007 Great Financial Crisis.

Unfortunately, John Templeton didn’t live to pick up the cheapest stocks in 2009. But if he were alive today, I have no doubt he’d be ringing the alarm bell.

Ten years into the longest bull-market in history, stocks have only been more expensive twice in the last 100 years.

Sir John Templeton

But just because the US stock market is overvalued, it doesn’t mean that there are no more safe and lucrative opportunities around… You just need to know where (and how) to look for them…

And just like John Templeton realized decades ago, some of the best opportunities today are found outside the United States.

Take Japanese-based Kitagawa Industries, for example. Investors generated 249% in just 17 months while taking minimal risk.

It’s a boring business and not as exciting as the latest high-flying tech IPO. Its main business is to produce equipment for the IT industry. So don’t expect to be the center of attention at a dinner party talking about it.

But it’s a mature company with a strong track record of profitability… And when we bought it, it was trading at a LARGE discount to the value of its assets. So large in fact, that the value of all the company’s shares was LESS than the company’s net cash.

In other words, investors were able to buy $1 for just $0.76. This made it an excellent investment.

When you buy shares of high-quality companies that are this severely undervalued by the market, you significantly reduce your risk and open yourself up to extraordinary profits.

This strategy is called Value Investing and it has been proven to be one the most successful investment strategies in the world. And it’s no surprise that it’s also the strategy of choice for Warren Buffett, one of the most successful investors in the world.

In this in-depth article you’ll learn how to find and invest in these kinds of opportunities no matter what the markets are doing. It could very well be the most important piece of financial education you ever read.

In this In-Depth Article

- What is value investing

- Data that PROVES value investing is one of the most successful investment strategies in the world

- The required mindset to execute a winning value investing strategy

- Investing rules to boost returns AND mitigate risk

- Just what is a “value investment”?

- How to find value investment opportunities

- How to vet value investment opportunities

- Case study of a successful value investment - How we made 249% in just 17 months

What is value investing

The ethos of value investing is simple: buy high quality businesses managed by competent people of integrity at valuations that are as low as possible.

It’s an intuitive idea to understand. We all love the feeling of getting a lot for our money– such as when we find incredibly cheap business class airfare or a huge discount on a new car.

The core idea of value investing is to essentially buy a dollar for 80 cents.

As value investors we determine the intrinsic value of a company and only purchase shares when the price is below that amount.

Warren Buffett famously said “Price is what you pay, value is what you get.“

At Sovereign Man’s flagship investment service, The 4th Pillar, where I’m the editor, we invest in deeply undervalued and massively overlooked companies.

So deeply undervalued in fact, that the shares of the companies I typically recommend trade for less than the amount of net cash they have in their bank accounts— just like what happened with Kitagawa Industries.

What it means when a company is trading for ‘less than net cash’...

If you were able to buy the entire company, you could immediately pay off all of the company’s liabilities, withdraw the amount you paid from the company’s bank account and additionally pay yourself whatever is left as a profit. Plus, you could sell all of the remaining assets and pocket that too.

Of course, nobody in their right mind would ever agree to such a deal. But sometimes the stock price of publicly traded companies is so irrationally beaten down that you can buy their shares well below the amount of cash they have on hand.

And when you buy stock at such a big discount, you significantly reduce your risk while at the same time increase your potential profit.

It sounds unreasonable that companies would trade this much below their intrinsic value… and you’re right, it is unreasonable.

But it still happens from time to time. Why? Because despite the drivel that they teach at most business schools, markets are NOT EFFICIENT– they are comprised of highly emotional participants.

Consequently, great buying opportunities emerge from time to time when the market becomes scared or otherwise irrational.

But sooner or later assets return to their intrinsic value. Overvalued stocks crash and the price of undervalued companies increases.

That’s why buying shares at a discount provides you with a significant margin of safety and reduces risk.

It’s a simple strategy. And although it’s simple, it’s not easy… It requires patience, common sense, and good old fashioned hard work. Attributes that many investors frankly lack.

But in return you are rewarded with reduced risk and exceptional profits.

For example, members of The 4th Pillar took profits of 303% on Carnarvon Petroleum, 58% on Nippon Antenna, 249% on Kitagawa Industries, 111% on Nam Tai Properties, 89% in Karoon Energy, 90% in Yorkey Optical and 57% on Mount Gibson.

And we’re not the only ones who have success with this investment strategy…

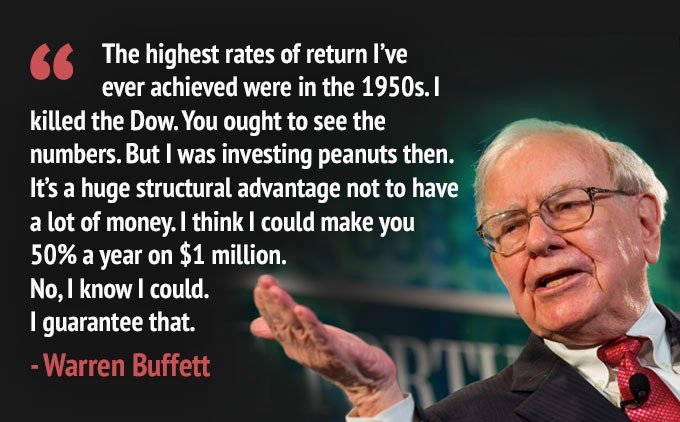

Value investing is how Warren Buffett became one of the wealthiest people in the world

Warren Buffett is the only investor among the world’s wealthiest people.

And he became enormously wealthy over his career specifically from value investing.

Since Buffett starting trading stocks at an early age, he bought $1.00 of value for 50 cents. And then he repeated, and then he repeated. Over decades, this approach grew Buffett’s Berkshire Hathaway holding company to more than 60 companies and current assets of $739 billion.

But you don’t have to be the next Buffett to benefit from value investing. This is a proven investment strategy that can work for any investor.

I'm sitting on 10 MORE opportunities similar to Kitagawa Industries that generated us 249% in just 7 months...

I’m not just Sovereign Man’s Chief Investment Strategist, but also the editor of our flagship investment service– the 4th Pillar.

Inside, I share all of my best value investment recommendations. And right now we are celebrating the release of our 100th issue with a generous 50% discount for new members.

The 4th Pillar has posted a 96% success rate since 2015– we made a profit on 26 out of 27 recommendations.

And right now we have 10 open recommendations trading at BUY levels…

Including a deeply undervalued company that is enormously profitable… and pays an eye-watering 15% dividend to its investors.

This is the first time in over six months that we are offering a discount on the 4th Pillar.

We won’t keep it open for long. So take a look right away...

Data that PROVES value investing is one of the most successful investment strategies in the world

In his book What Works on Wall Street, James O’Shaughnessy compared the returns of different investment strategies over a period of 52 years.

He found that value investing vastly outperformed other strategies.

He used a period of 52 years to make sure that the conclusions apply over the long-term and cover different economic and business cycles.

And although this strategy does require a little bit of patience, it generates fantastic returns even in the short-term. Kitagawa Industries we mentioned is a fantastic example that generated 249% in just 17 months.

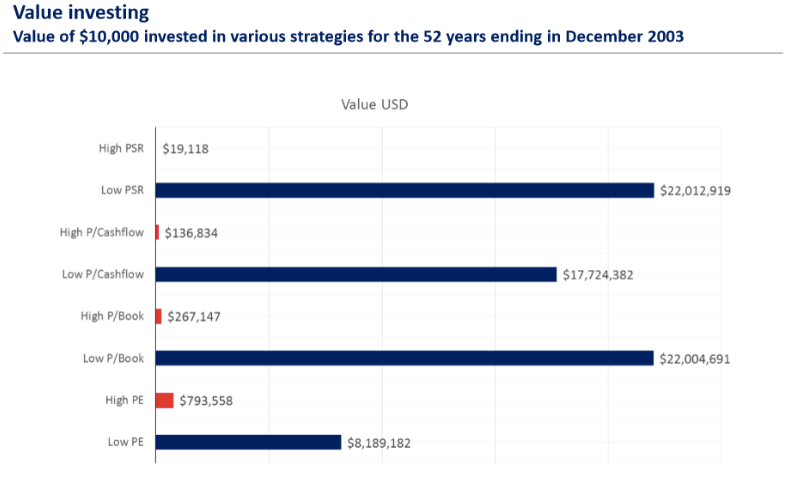

Here’s how O’Shaughnessy determined value investing vastly out-performed other strategies

A common way to measure whether a stock is expensive or cheap is the price/earnings (PE) ratio. It shows you how many years of a company’s earnings it would take to pay back the purchase price.

Netflix currently trades at a PE ratio of 128, for example. This means that if you bought the entire company, it would take you 128 years to get your initial investment back– provided you pocketed all the profit and didn’t reinvest any of it back into the business.

First let’s look at a non-value oriented strategy…

If you had invested $10,000 in the 50 stocks with the highest PE ratio 52 years ago, your investment would be worth $793,558 today.

Not a bad result at first glance. This is comparable to what growth investors and index funds are doing today in the overvalued US market when they invest in expensive stocks such as Netflix or Tesla.

However, Value Investing would have generated 10-27x higher returns

But let’s compare this approach to a more value oriented strategy of buying the 50 cheapest stocks with the lowest PE ratio instead of the highest over the same period…

Your investment would be worth $8,189,182. That’s over 10x more than the high PE strategy.

Another popular valuation method – especially amongst value investors – is the price to book ratio. This is essentially a reflection of how much an investor is paying relative to the value of a company’s “net worth.”

Remember, as a value investor you always want to pay the lowest price possible for a company compared to its intrinsic value.

So if you had invested the same $10,000 in the 50 stocks with the lowest price/book ratio your investment would be worth an astonishing $22,004,691. That’s over 27x more than the high PE strategy.

You can see a comparison of the strategies in the chart below.

The blue bars are value investment strategies and the red bars are conventional, non-value oriented strategies.

As you can see, the best performing strategies, by far, were all based on value investing.

These results really shouldn’t be a surprise. When you buy the highest quality assets at the cheapest possible price, you’re maximizing your chance at outsized investment returns.

But you might be wondering…

If value investing is so effective why isn’t EVERYONE doing it...

First of all, value investing is a simple strategy, but not an “easy” one.

It requires a lot of patience and the willingness to go against the grain. Oftentimes it can take a while for the rest of the market to realize that the shares are massively undervalued. Many investors are simply not patient enough.

Another reason is that during long bull markets there are fewer and fewer undervalued companies left. Today, for example many of the undervalued companies I find are relatively small and can only absorb a small amount of capital.

But large institutional investors (hedge funds, insurance companies, pension funds, etc.) manage billions or even trillions of dollars. They simply cannot buy large numbers of shares in smaller companies without substantially raising the share price. They are limited to investing in large, popular companies like Apple that can absorb these large pools of capital.

That gives you and I a SIGNIFICANT advantage and leaves us with the best deals.

We can discover value in less liquid, smaller stocks. Our stocks don’t attract nearly as many eyeballs as Coca-Cola or Apple, for example. There’s not as much price discovery happening daily, which can be to our advantage.

That’s exactly why Warren Buffett said…

To get started, all you need is a little education and the right mindset.

The required mindset to execute a winning value investing strategy

Financial markets are like any other market – a collection of buyers and sellers, governed by the laws of supply and demand.

If you’re buying when everyone else is buying or selling when everyone else is selling, it’s difficult to gain an edge.

But breaking away from the investing herd can be a difficult thing to do.

Thousands of years ago, going against the clan or tribe could mean compromising the group or your own death. You’d think that our brains would adapt to the modern world that’s not exposed to daily danger. But unfortunately, we still carry that herd-like mindset from ages ago. And it’s potentially stifling your investment returns.

Instead, I encourage you to adopt a countercyclical perspective: Buy when things are on sale, and hold until the market rushes in.

But you can’t simply buy an asset because it’s on sale.

There are numerous reasons for why a company’s share price may appear undervalued. Maybe the company is hemorrhaging cash. Or, the management could have taken on too much long-term debt relative to its assets.

Maybe revenue and earnings have taken a hit recently, and management hasn’t addressed shareholders’ concerns that a turnaround is imminent. Maybe it’s a “sunset” industry. Perhaps management has a bad reputation, or are known to be unethical.

As value investors we largely disregard what’s happening in the greater economy. It’s not a concern if interest rates are rising or falling, or if GDP growth is 2% or 5%.

Instead, value investors focus on the company’s balance sheet, its long-term profitability, its dividend, its management, its adaptability to changing customer demands and preferences, and so on.

Usually, there are overlooked and available stocks that meet these criteria trading in some corner of the world.

Still, if trading markets was this easy, everyone would be making money.

Behind all this trading in financial markets is irrational human action, which makes markets risky and often unpredictable.

People often don’t operate like you think they would, if they were acting rationally. They buy when financial assets rise in price. They panic sell when asset prices fall.

So, profitable investing takes much more than the right mindset.

You need a deep knowledge of markets and some rules to invest by. I’ve developed a strict set of rules that separate average investments from the most compelling ones…

Investing rules to boost returns AND mitigate risk

Whether you’re an individual investor or professional money manager, rules are crucial for any investor and all types of investing approaches.

So, here are the three basic – and correlated – investing rules that I live by:

- 1.Be on the lookout for low-risk trades, because they are always around;

- 2.The primary focus of any investment - don’t lose money;

- 3.Always consider the downside risk of any potential investment first

You can be confident that when I invest in any stock, I’ve first carefully considered the risk-adjusted return. For example, if there’s an opportunity to make 10%, but the downside risk is 40%, then it’s an obvious pass.

But markets also present opportunities for the exact opposite risk-adjusted return. And deep value stocks can tip the odds for a profit in your favour.

So, with this focus on the downside risk and rules in place, next I trust metrics that let me know if a company is undervalued and an attractive investment…

Just what is a “value investment”?

When you buy shares of a company, you become an owner of that business. And you want to make sure that the business is financially sound.

The ratios below can help us determine if a company is overvalued or undervalued. And value investors can focus on a number of metrics.

These include, but are by no means limited to:

- Price to Earnings (P/E) ratio

- Price to Book (P/B) ratio

- Price to Net Cash ratio

In each case, price is easy. It’s the current share price or market value, determined every day by shareholders exchanging shares on the New York Stock Exchange, Nasdaq, or all the stock markets around the world.

Each publicly traded company is required to publish its financial statements – its balance sheet, income statement and cash flow statement. There you can find the values to calculate the ratios below.

Price to Earnings (P/E) ratio

This is one of the most commonly used valuation ratios.

It shows you how many years of a company’s earnings it would take to pay back the purchase price.

To calculate the Price to Earnings (P/E) ratio, you’ll need to refer to the company’s income statement.

Earnings are the company’s profits, also known as the after-tax income – the revenue less expenses and other accounting factors, like depreciation and amortization.

From a value investor’s perspective, the lower the Price to Earnings Ratio the better.

Price to Book (P/B) ratio

The Book Value is essentially the company’s “net worth”. It is defined as a company’s Total Assets less its Intangible Assets (goodwill and patents) and its Total Liabilities.

Book Value can give you an idea of the company’s liquidation value. In other words, it’s the value of a company’s assets should the business close down and be sold off.

And the Price to Book ratio is essentially a reflection of how much an investor is paying relative to the value of a company’s “net worth”.

It’s a very popular ratio for value investors. The lower it is, the better.

For example, when the shares of a company are trading at P/B ratio of less than 1 it means that you are paying less than the tangible value of the company.

But my personal favorite ratio is the …

Price to Net Cash ratio

It’s the metric around which our flagship investment service, The 4th Pillar, is based.

To find Net Cash, you first look at the top line of the company’s Assets: Cash and Cash Equivalents. (A balance sheets lists the most liquid assets – Cash and Cash Equivalents – first.)

Next, find the company’s Total Liabilities.

Third, calculate Net Cash. You’ll take that Cash and Cash Equivalents number and subtract the company’s Total Liabilities.

Now, you need to calculate the Net Cash per share. So, take the number you calculated just above and divide by the number of shares outstanding. You can find the number of shares outstanding in any annual or quarterly report, usually uploaded on the company’s investor relations page, or by referencing a website like Yahoo Finance, Google Finance, Bloomberg, or Reuters.

Finally, you’ll compare this Net Cash per share number with the company’s current share price. Sometimes, though very rarely, a company trades at a discount to its Net Cash per share. That means you could theoretically buy the entire company’s assets, close the company, liquidate everything, and still put money back in your pocket.

You’d never get this type of investment opportunity in a private transaction. A business owner would first pocket his or her money and only then sell you the business.

So, if a company trades at a discount to Net Cash per share, this could be a great investment opportunity.

But this is only the beginning of my analysis. Remember, just because a stock is undervalued, it doesn’t mean that it’s a good investment. You also need to make sure that it’s a good business in the first place

But before we get to that, let me show you…

How to find value investment opportunities

It’s difficult to find anything of value in large US stocks.

By nearly every metric, the US stock market is fully priced. For example, the S&P 500’s price to earnings (P/E) ratio is the second highest in history. The cyclically adjusted price to earnings ratio (CAPE) – the average inflation-adjusted earnings from the previous 10 years – is at nearly 30, about double the median of 15.7.

As a deep value investor, this doesn’t interest me in the least.

You’ve got to look for value in other markets, places where many US investors are afraid or unwilling to go.

Fortunately there are tools, called screeners, that can help you filter stocks from around the world based on financial metrics and investment criteria.

You can run various screens to whittle down the list from thousands of stocks to a more manageable number that you can then individually analyze.

There are some free screeners around, such as finviz and MSN’s stock screener.

But I prefer Gurufocus, because it has very comprehensive coverage of most global markets and allows me to screen at a very granular level. At $2,071 per year for all regions it’s not cheap, but for me as a professional it’s a reasonable expense.

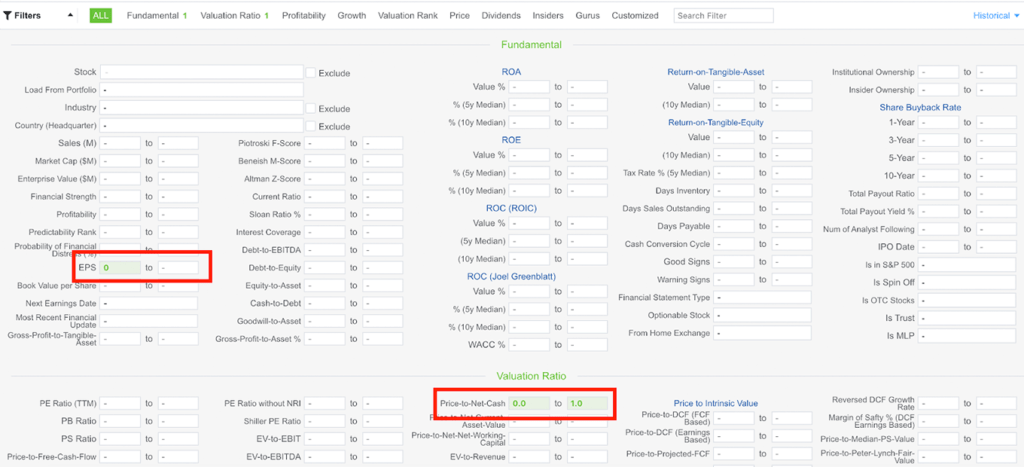

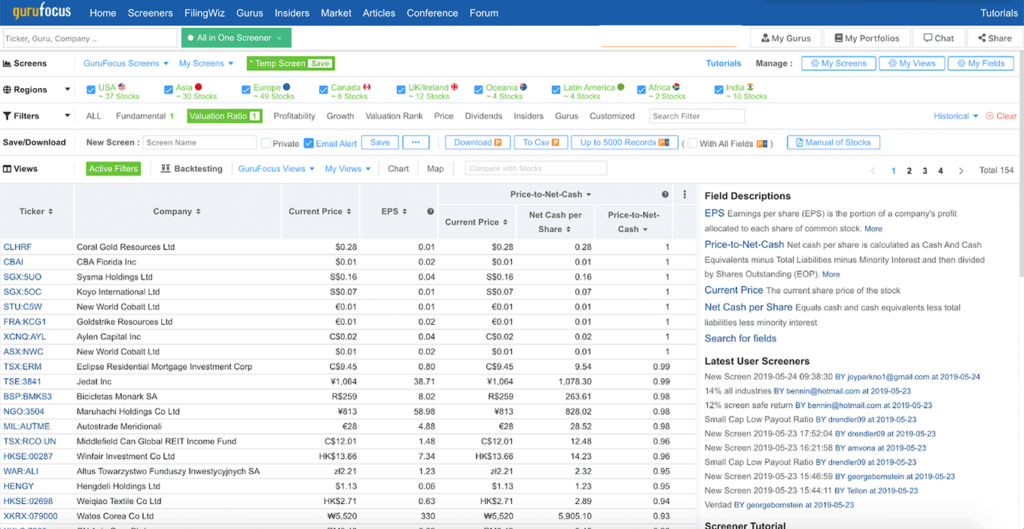

How to use gurufocus to find potentially undervalued companies

Visit the Gurufocus Screener website. You can get a 7-Day free trial to practice the process below.

As a starting point you can set the following two filter criteria to get a list of potentially lucrative undervalued opportunities:

1. Price-to-Net-Cash

Set it to higher than zero and equal to or less than one.

This criteria allows you to filter companies that are currently undervalued.

When an entire company is valued at less than the amount of the net cash it has in the bank, it gives us a significant margin of safety. This is a very conservative deep value strategy and the one I am using for many of the recommendations in The 4th Pillar.

At the time of publishing there were only 154 companies worldwide that meet this criteria and have positive earnings.

Alternatively, you could also filter for companies that are trading for less than their book value (the value of all tangible assets) for a less conservative valuation method. That gives you a wider selection of businesses to analyse in more depth.

2. Earnings per share (EPS)

Set it to from zero to unlimited.

This makes sure we only filter for companies that are profitable.

We are only interested in decent, profitable businesses that are mispriced by the market. We don’t want to invest in companies that are losing money and likely to have a low valuation that’s justified by their financial performance

You will get a list of potential opportunities like this…

But my work doesn’t end there.

Finding the companies that fit the criteria is the easy part. The harder part is ensuring that these stocks are legitimate. And there’s no shortcut or easy button that reduces a few dozen stocks to only the best, worthy of a 4th Pillar recommendation.

So, my elimination process begins… by reviewing each stock, one-by-one.

How to vet value investment opportunities

Again, just because a stock has made it through all my screeners doesn’t mean that it’s a good investment opportunity.

I execute a process that helps me separate the few dozen opportunities from the recommendations I can stand behind.

1. The company’s corporate management

First, an easy eliminator is a company’s corporate management.

There’s one company – G-Resources – that regularly meets all the criteria in my screens and shows up on the short list each month. Just by looking at the company, an individual investor probably wouldn’t know to eliminate this option because of unethical management.

But between studying the company and my trusted financial management network, I know that the company’s management is not to be trusted.

Usually, but not always, companies with less than ethical corporate management cannot remain in business for decades. So, when I’m filtering through this list of companies, those that have been operating for many years is a plus. Again, it’s not a fail-safe, but these companies likely have no unethical management issues.

Also, incentives for the company’s management and shareholders must align.

I favour companies where managers have significant ownership stakes in the company and thus think like owners. Since we’ve already checked that the executives are not unethical, I’m confident that they’ll only take legitimate (i.e. legal) steps to raise the company’s share price. And shareholders will benefit.

2. The company jurisdiction

Next, I check where the company is based.

Of course, there’s some nuance here. Just because a country is renowned for not upholding securities laws doesn’t mean that there are not opportunities there. Likewise, just because a country abides by securities laws doesn’t mean that there are not less than respectable companies there.

But the safe bet is to focus on companies located in jurisdictions that uphold the law and have robust corporate governance in place. So, Australia, New Zealand, Hong Kong, Japan, South Korea, etc. are all options.

If the company is domiciled in one of these countries, then I move on to review and analyze each remaining company’s financial statements.

3. The company’s financial statements

Here, I’m checking to ensure that there’s no anomalous data was pulled into gurufocus.

I always cross reference the data the screener shows with the company’s own public disclosures. Remember, the margin of safety needs to be there for us to move ahead.

For those stocks still in the running, rather than rely on secondary news sources, I go straight to the company’s website or to the stock exchange to read financial disclosures and other company announcements. I spent some time in South Korea, so having that language skill comes in handy for the Korean companies.

By this time, I’m usually down to a handful of companies.

Another consideration is WHY the company is so severely undervalued.

Is it simply overlooked or out of favor by an irrational market, or is there an underlying business factor that’s driving the share price down? Is it cyclical? Or, is it structural? In other words, is something temporarily out of favour, or terminally in decline?

For example, the US-traded company Gamestop is a video game and consumer electronics retailer. In an age of increased streaming and relentless competition, Gamestop’s share price has taken a nosedive. Gamestop may be undervalued, but it’s undervalued mainly because it hasn’t adapted to changing consumer preferences and its financials have been undermined as a result.

To borrow a metaphor – Gamestop is a buggy whip manufacturer when people are increasingly abandoning horses and buying cars.

Examining a company’s revenue and earnings helps to ensure the business isn’t a buggy whip manufacturer. Positive trends also tell me that the company is making necessary adjustments in capital expenditures and operating costs.

Ideally, a promising company will have several years, or even better, a decade or more of increased revenue and earnings.

Over on the balance sheet, although not a requirement, I like to see companies that have little or no long-term debt. Remember, long-term debt is already counted in the company’s Total Liabilities and its Net Cash per share calculation.

But without any long-term debt, a company can wisely deploy capital to grow market share or invest in the success of the business. Either way, this increases our chances of seeing a higher share price down the road. The company could be a takeover target or any number of other catalysts could translate into big profits for shareholders.

4. Shareholder composition & analyst sentiment

I also examine the shareholder composition.

Investors or institutions who have a 5% or greater stake in a company’s shares must disclose this fact in a government filing. It’s good to see investment companies and pension funds invested – parties who have a vested interest in the long-term success of the company.

Of course, for shareholders to benefit, there has to be plenty of room for them to enter a position in the first place.

This is called the company’s “float” – the percentage of shares issued to the public out of the company’s total outstanding shares.

Usually, a small float only becomes an issue for companies that recently started trading, so it’s not a factor for us. But it’s still a part of my checklist for well-established companies. If the small float is due to the company being closely held by the founders, or the family that has owned it for generations, that’s actually a GOOD thing, in general.

As I mentioned earlier, it’s wise to adopt a countercyclical mindset for investing success.

So, I also dig up the analyst sentiment for a potential investment. These are individuals employed by major banks to know the ins and outs of the company. When all signs are pointing to a great value investment but analysts are negative on a stock, perversely that’s often an encouraging sign that it’s a buy.

5. Dividends

Despite being right about a value stock, it can take months or sometimes even years for it to turn in our favour. For this reason, it’s nice to collect dividends while we wait for a catalyst. Dividends are not absolutely required, but this fact can separate my top contender from the rest of the pack.

Even a small dividend yield – the cash dividend per share divided by the share price – of 1% can give us a little cash in the meantime. Plus, if the company still pays a dividend despite a depressed share price, they’ve made a commitment to shareholders.

You can imagine that after I scrutinize the stocks along these lines, only a few options remain.

And I can then select the single best out of this bunch as a new 4th Pillar recommendation… just like Kitagawa Industries.

Case study of a successful value investment - How we made 249% in just 17 months

Back in 2017 when I initially recommended Kitagawa, the company had Y1,453 (US$13.26) per share in net cash.

I recommended buying shares at Y1,110 (US$10.13) or better. That’s a healthy 24% discount.

Kitagawa continued to report healthy profits. Also, the company twice paid a Y6 (US$.055) per share dividend. That was less than a 1% yield, but still some income while subscribers awaited the catalyst for an increased share price.

But throughout 2017 and most of 2018, Kitagawa stayed within a fairly tight trading range. It took some patience for subscribers to stick with the recommendation, while we waited for that catalyst. And then it came…

In late 2018, a competitor in the electrical and mechanical equipment industry looking for an easy way to grow approached Kitagawa making a takeover (or tender offer, as it is under Japanese securities laws).

The price the acquirer offered was Y3,943 (US$35.98).

Kitagawa’s products aren’t exciting, but the company has a strong track record of profitability. And that’s what matters to us as investors.

To the company taking over Kitagawa in a “going private” transaction, the business was worth 3.5 times what the shares were languishing at when 4th Pillar subscribers first bought them, below cash backing.

Subscribers exited at Y3,915 (US$35.72) or better – with those two dividends, at least a 249% gain.

Over the same timeframe subscribers held Kitagawa stock (again, July 2017 until December 2018), the S&P 500 returned about 15%… and that’s if investors didn’t panic sell at depressed levels through the volatile Q4 2018.

Clearly, deep value investing paid off for our subscribers with Kitagawa stock.

I’ve spent decades analyzing these types of value plays and honing my craft (learning to separate the garbage from the winners).

And the results speak for themselves…

Since the beginning of 2015, 95% of my closed recommendations have been winners.

I hope this article was valuable for you and I wish you a lot of success in your investment journey.

Value Investing is a simple strategy… but it is not easy. It requires patience and a lot of hard work.

Fortunately, you can…

Let Me Do All The Hard Work For You…

By accessing ALL my best recommendations in The 4th Pillar at 50% OFF

I’m not just Sovereign Man’s Chief Investment Strategist, but also the editor of our flagship investment service– the 4th Pillar.

Inside, I share all of my best value investment recommendations. And right now we are celebrating the release of our 100th issue with a generous 50% discount for new members.

The 4th Pillar has posted a 96% success rate since 2015– we made a profit on 26 out of 27 recommendations.

And right now we have 10 open recommendations trading at BUY levels…

Including a deeply undervalued company that is enormously profitable… and pays an eye-watering 15% dividend to its investors.

This is the first time in over six months that we are offering a discount on the 4th Pillar.

We won’t keep it open for long. So take a look right away...

How did you like this article?

Click one of the stars to add your vote...

Other readers gave this article an average rating of 5 stars.