Earlier this week we talked about why the economic consequences of this pandemic could last a lot longer than what a lot of people expect.

Now, I say all of this from a position of complete ignorance and uncertainty. Nobody knows what’s going to happen next, or how long this pandemic will last.

But to simply expect that everything will return to normal in a few weeks– and willfully ignore the countless other possibilities– seems a bit foolish.

Worldwide, the number of deaths from Covid-19 reached 138,000. That’s more than double the number of deaths from 10 days ago. So it’s still growing.

Singapore was initially successful in controlling the virus outbreak. But they’re now experiencing a nasty second wave of infections.

In the US alone, more than 20 million people have lost their jobs so far, and the government’s $350 billion program to bail out small businesses has already run out of money.

It’s great to hope for the best. But let’s be realistic: there are a lot of reasons why the economic consequences of this pandemic could be long-lasting.

And that’s what brings me to real assets.

If the negative consequences linger, it’s reasonable to expect that governments and central banks will shovel piles of cash into their economies at a feverish pace.

Most developed nations have started this already.

In Australia, the government has passed at least $130 billion in stimulus measures so far– a princely sum in a country where the population is just 25 million people.

The British government has passed hundreds of billions worth of loan guarantees, grants, and tax cuts.

Germany’s government has passed more than 750 billion euros worth of loans and stimulus programs.

Canada’s central bank slashed its benchmark interest rate to 0.25%, and cut bank reserve requirements, in addition to billions of dollars in stimulus programs.

And the United States government has spent trillions of dollars already; plus the Federal Reserve has conjured more than a trillion dollars out of thin air to loan money to banks and businesses.

It’s likely they’ll keep printing money if the economic pain persists.

Second wave of outbreaks? Print another trillion dollars to bail out businesses.

Massive corporate layoffs? Print another 2 trillion dollars to bail out employees.

Skyrocketing loan defaults? Print another 5 trillion dollars to bail out the banks.

Now, consider that they’d be printing all this money at a time when economies are shrinking by 20% or more.

So we’d see a tidal wave new money flooding into an economy where fewer goods and services are being produced.

This is precisely how a currency loses value: if there’s less stuff in an economy, but more paper money, it means all the stuff has to become more expensive relative to the paper money.

That’s ultimately what inflation is.

Throughout history whenever this situation has arisen, it’s almost invariably been a good idea to own real assets, i.e. direct ownership of an asset that cannot be conjured out of thin air by a central bank.

Real assets include things like productive land, shares of a well-managed private business, or physical gold and silver.

These are assets that cannot be willed into existence by a government or central bank. And they don’t simply exist on paper, or as an entry on a balance sheet.

They’re real. And they tend to do very well in an inflationary environment where ridiculous sums of money are being printed.

Most people don’t have an easy opportunity to buy productive land or shares of a well-managed private business.

But gold and silver are totally within reach. And here’s something really interesting about them:

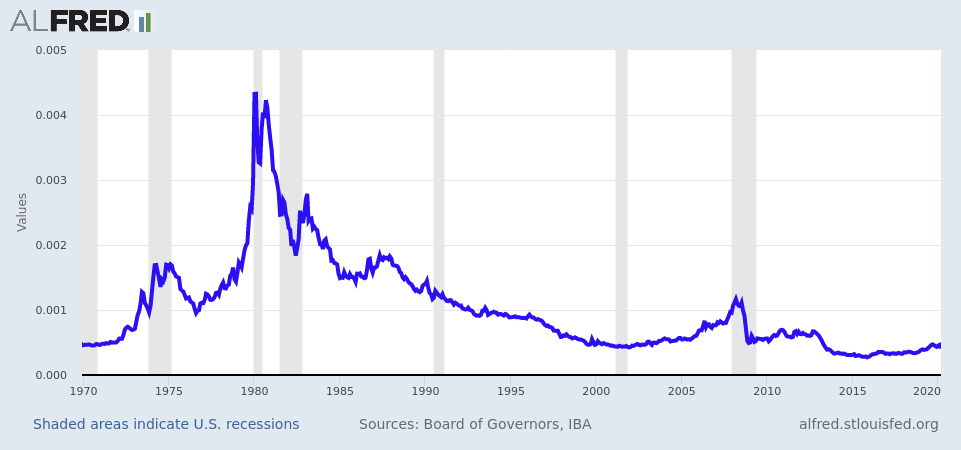

The chart below shows you the ratio over the past 50 years between the price of gold and the “M0 monetary base”.

As you can see, right now this ratio is well below its long-term average.

(M0 is just one method economists use to measure the supply of money in the US economy. But using other methods, like M2 money supply, the ratio is still below its long-term average.)

This low ratio suggests that the gold price is cheap relative to the amount of money in the economy right now. And it stands to reason that the amount of money in the economy is going to increase a LOT.

And that means the price of gold could also increase a lot.

But if gold is relatively cheap, silver is even cheaper.

As I wrote to you on Monday, the gold / silver ratio is near an all-time high. In other words, it takes twice as much silver to buy a single ounce of gold relative to the long-term average.

So while there’s a good case that the price of gold can increase quite a bit, it’s possible that the price of silver could rise even more.

There are, of course, risks. Nothing is certain, especially in this environment.

But there are some inexpensive ways to bet on rising gold and silver prices where you could make potentially 10x your money or more, even with limited amounts of capital.

We’ll talk about these next week.

For now, stay safe and healthy.